The methodology of utility analysis is used as an example to show how strategic management decisions for or against Digitization of business processes can be made and implemented. To this end, the application example of incoming invoice verification is used, whereby the status quo of manual incoming invoice verification is compared with automated electronic processing by means of a utility value analysis. The result of the utility value analysis should provide an answer to the question of whether and how the process of incoming invoice processing can be made paperless and efficient electronically.

Decision-making through benefit analysis: the need for process digitization

The introduction of electronic invoice processing is accompanied by far-reaching changes to existing structures, processes and fields of activity that require suitable change management. The benefit analysis is a suitable instrument that, on the one hand, presents the additional benefits of an alternative and, on the other hand, involves all employees affected by a change across departments from the outset. In particular, the fact that several stakeholders are involved in the decision-making process makes the method objective and the resulting decision enables a high level of acceptance. In this respect, the benefit analysis offers a suitable instrument for participative, joint, objective decision-making and thus ensures commitment to the implementation of the decision.

How the utility analysis works

The benefit analysis focuses not only on monetary aspects, but in particular on the functional benefits. It is used for assessment in the context of decision preparation and allows both quantitative and qualitative criteria to be taken into account. The analytical and systematic approach should be particularly emphasized, so that it can be used in particular to solve complex decision-making problems.

Derivation of comparison criteria

In the first step of the utility analysis, the criteria to be considered in the evaluation are selected and a target system is set up. It is recommended that the target structure is built up in stages and hierarchically, so that higher-level targets or groups of criteria are concretized with the help of sub-targets. The following points should be noted:

- CompletenessConsideration of all quantitative and qualitative criteria that influence the benefit

- Freedom from overlap: similar objectives are to be combined

- Preference independence: there must be no dependency between the objectives

- ManageabilityConsideration of a maximum of seven criteria

- Avoidance of "must targets"their fulfillment is a basic requirement

- Applicability of the criteriamust be adapted to the status quo and alternative

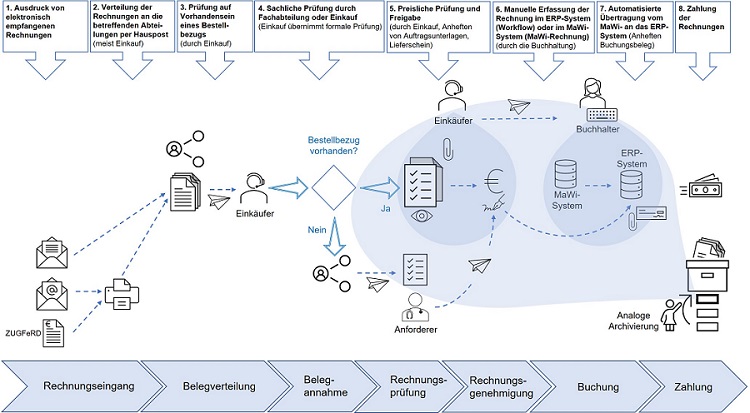

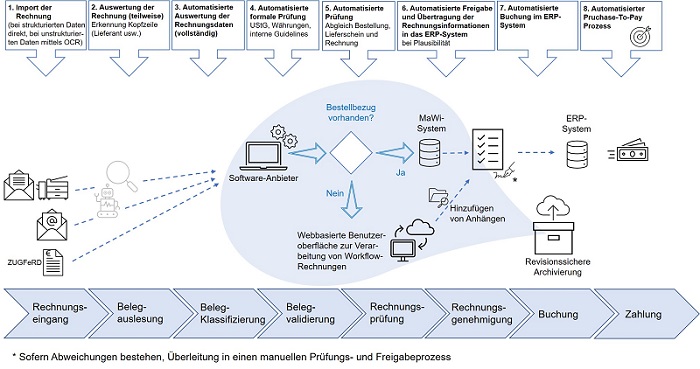

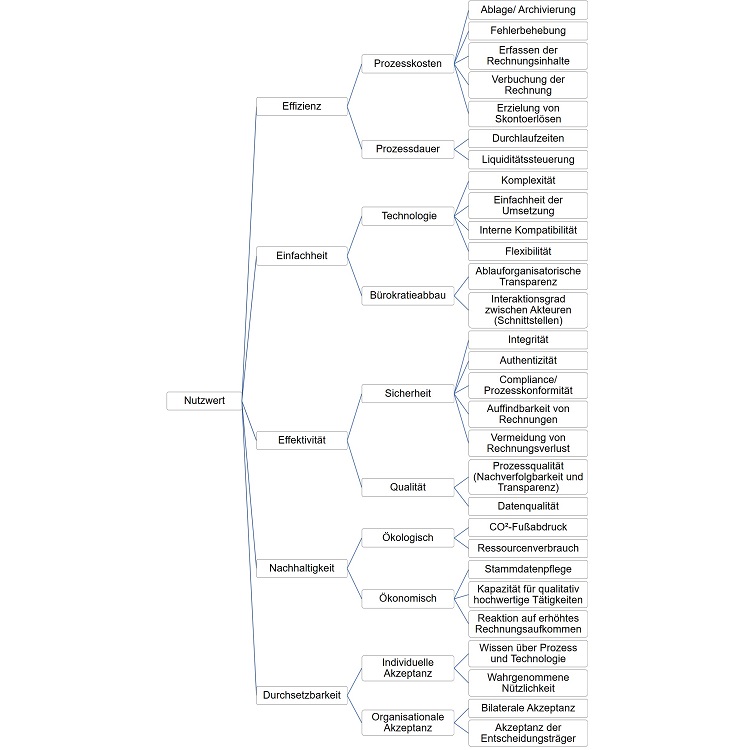

The criteria to be considered for the benefit analysis can be derived from the problem, the differences and the advantages and disadvantages of analog and electronic invoice processing (see the two figures above). There are five overarching objectives for invoice processing, the benefits of which are in turn made up of sub-objectives. These are efficiency, simplicity, effectiveness, sustainability and enforceability.

Efficiency

Efficiency has two characteristics. On the one hand, it is reflected in the process costs and, on the other, in the process duration.

The following fall under the aspect of legal costs

- Efficiency of filing and archiving.

- Effort for reading and recording the invoice content

- Expenses for the formal and factual verification of an invoice

- Possibility of generating cash discount income

- Effort for troubleshooting.

In terms of process duration, two key criteria can be identified for the efficiency comparison:

- Processing time of an invoice

- Liquidity management options.

Closely linked to the cost aspect of lost cash discount income is the ability to manage liquidity in a targeted manner. This is only possible if an overview of all outstanding invoices is available at all times. Furthermore, it is only possible to influence the time at which an invoice is settled if there is still sufficient time left until the payment deadline after an invoice has been released, which is why the aspect of liquidity management can be categorized under the overarching goal of process duration.

Simplicity

The criterion of simplicity can be divided into a technological and a bureaucratic dimension. Among the technological point of view In addition to internal compatibility, the key criteria are simplicity of implementation, flexibility and complexity. Flexibility refers to the customizing of the software solution and the ability to adapt to changes at short notice. If software solutions are highly fragmented, technical implementation is difficult. The more interfaces there are, the more complex the implementation. Internal compatibility refers to the additional functions that go beyond the core benefits of a solution, such as the ability to create evaluations. The criterion of technological simplicity describes, for example, the ergonomics of the user interface.

The one on the Reducing bureaucracy The second part of simplicity is reflected in the degree of interaction between the players. The fewer people involved in a process, the fewer interfaces there are and the less bureaucratic the procedure is. On the other hand, the organizational transparency of the process also has a direct impact on reducing bureaucracy.

Effectiveness

The criterion of effectiveness has two aspects: Safety and quality. The aim of Security This is reflected in the possibilities for circumventing processes, the traceability of invoices and the prevention of invoice loss and data manipulation.

The qualitative nature of effectiveness is reflected in the Process and data quality. Process quality includes the criteria of traceability and transparency. In the electronic process, these are fulfilled by the fact that each processing step is documented in an approval or document history and the location of an invoice for processing is transparent at all times. Invoice errors and input errors are summarized under the aspect of data quality. The advantages of an automated solution are particularly evident in repetitive data entry tasks, as it produces significantly fewer errors.

Sustainability

The fourth superordinate Sustainability criterion in turn has two components. Ecological sustainability includes the ecological footprint in the form of emissions and resource consumption. Electronic dispatch and digital processing support the reduction of emissions both through electronic dispatch and through the elimination of the production of the paper document itself.

The Economic sustainability aspect is reflected in the possibilities for master data maintenance, the ability to react to an increased invoice volume and the capacity for higher-value activities of the employees involved in the process. The quality of the master data has a direct influence on the duration of invoice verification. The better the quality, the fewer deviations and the less manual correction work required. However, acting in an economically sustainable manner not only means ensuring continuously improving master data quality, but also using existing resources where they are most beneficial. In the case of manual invoice processing, one full-time employee in the company studied is almost 100% occupied with repetitive tasks such as entering invoice content. There is no time to perform higher quality tasks that are meaningful for the employees. If, for example, a robot were to take over this task, the employee could spend more time on other, value-adding activities. Another aspect is the ability to react to a higher volume of invoices. With electronic invoice processing, temporary peaks as well as a permanent increase in invoice volume can be easily compensated for.

Enforceability

The last target category is enforceability, which is defined in individual and organizational acceptance is expressed. The latter refers to the acceptance of decision-makers and business partners. Large suppliers in particular have a vested interest in the electronic dispatch and digital processing of invoices, as they save on postage on the one hand and hope that invoices will be paid on time on the other. At management level, it can be assumed that digital invoice processing will be more widely accepted, as management is guided in particular by economic considerations.

Acceptance at the individual level of clerks is lower than the acceptance of managers. The introduction of electronic invoice processing necessitates a transfer of skills in financial accounting and requires employees to build up skills in terms of process knowledge and technological understanding.

Carrying out the benefit analysis

The basis for carrying out the utility analysis is the derivation of suitable comparison criteria. The subsequent steps of weighting and evaluation are characterized by strong subjectivity, so it is advisable to carry them out in a team. This not only promotes objectivity, but also supports the acceptance of the resulting decision. At the same time, tools such as the pairwise comparison can help to select a sensible weighting.

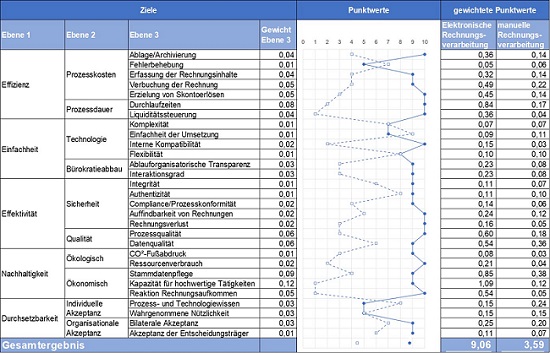

The following figure shows an example of a potential result of a utility value analysis for invoice processing using a profile representation. If the point values of the alternatives are closer to each other, it is advisable to develop different scenarios, for example by varying the weightings. The result of the utility analysis is only valid if it leads to the same result even if the weighting is varied slightly.

Conclusion

The benefit analysis is a suitable tool for comparing the status quo in terms of its qualitative benefits with automated processing and thus justifying a strategic management decision. As the benefit analysis is carried out as a joint participatory procedure between all actors involved in the process, it proves to be particularly suitable in the context of long-established settings and routine processes. The benefit analysis can help to create acceptance for decisions on the digitalization of processes.

This article was co-authored by Stefanie Albrecht and Professor Dr. Peter Steinhoff. Stefanie Albrecht completed her Bachelor's degree in Business Administration in Healthcare at the University of Applied Sciences in Neu-Ulm. She is currently working as a purchasing officer at a university hospital and is studying for a Master's degree at the University of Applied Management in Ismaning, specializing in International Accounting.

Bibliography

Andler, N. (2015): Tools for project management, workshops and consulting: Compendium of the most important techniques and methods. 6th ed., Erlangen: Wiley

Bernius, S./Pfaff, D./Werres, S./König, W. (2013): Recommendations for the implementation of electronic invoice exchange with public administration: Final report of the eRechnung project. Online: https://www.ferd-net.de/upload/Handlungsempfehlungen-Rechnungsaustausch.pdf (Accessed: 26.06.2020)

Bieg, H./Kußmaul, H./Waschbusch, G. (2016): Investment. 3rd ed., Berlin: Franz Vahlen

Burghardt, M. (2013): Introduction to Project Management: Definition, Planning, Control and Closure. 6th ed., Somerset: Publicis MCD Werbeagentur GmbH

Diehm, J./Benzinger, L. (2018): Digital Finance: Digital invoice processing and workflows as the basis for accounting 4.0. In: Der Betrieb (DB), 71 (15), pp. 841-847

Koch, S. (2011): Introduction to Business Process Management: Six Sigma, Kaizen and TQM. Berlin/Heidelberg: Springer

Schömburg, H./Breitner, M. H. (2010): Electronic invoices for optimizing the financial supply chain: status quo, empirical results and acceptance problems. In: Schumann, M./Kolbe, L. M./Breitner, M. H./Frerichs, A. (Eds.): Proceedings of the Multiconference on Information Systems (MKWI), 23-25.02.2010, Göttingen, pp. 1253-1264

Schön, D. (2018): Planung und Reporting Im BI-Gestützten Controlling: Grundlagen, Business Intelligence, Mobile BI und Big-Data-Analytics. 3rd ed., Wiesbaden: Springer Gabler. in Springer Fachmedien Wiesbaden GmbH

Schulze, U. (2009): Information technology use in supply chain management: A conceptual and empirical study of benefit effects and benefit measurement. In: Weber, J. (ed.): Schriften des Kühne-Zentrums für Logistikmanagement, vol. 10, Wiesbaden: Gabler

Svatopluk, A./Haisermann, A./Schabicki, T./Frank, S. (2018): Robotic Process Automation (RPA) in accounting and controlling - what opportunities arise? In: Controlling (CON), 30 (3), pp. 11-19

Vahs, D./Brem, A. (2015): Innovation management: From the idea to successful commercialization. 5th ed., Stuttgart: Schäffer Poeschel

Weber J./Schäffer, U. (2014): Introduction to management accounting. 14th ed., Stuttgart: Schäffer Poeschel

(Cover image: © makibestphoto | Adobe Stock)